Demand & Time Deposits: Differences, Advantages & Examples

In the world of banking, demand deposits and time deposits are two fundamental concepts that play a crucial role in managing personal and corporate finances. These deposits serve as key tools for saving, transacting, and earning interest, making them essential for both individuals and businesses.

In this article, we’ll delve into the details of demand and time deposits, their differences, advantages, and how they fit into modern financial planning.

What are Demand Deposits?

Demand deposits refer to funds that customers deposit into their bank accounts, which can be withdrawn at any time without prior notice. These deposits are highly liquid, allowing individuals and businesses to access their money on-demand for everyday transactions.

Features of Demand Deposits:

- Immediate Access: Account holders can withdraw funds anytime using ATMs, checks, or online banking.

- No Maturity Period: There is no fixed duration for holding funds.

- Low or No Interest: Demand deposits typically offer little to no interest, as they prioritize liquidity over returns.

- Common Types: Examples include savings accounts and checking accounts.

Advantages of Demand Deposits

- Convenience: Allows instant access to funds for daily needs like shopping, bill payments, and emergencies.

- Liquidity: Provides flexibility to manage finances without any restrictions.

- Security: Money is safely stored in the bank, reducing the risks associated with carrying cash.

- Ease of Transactions: Supports seamless transactions through checks, debit cards, and online banking.

What are Time Deposits?

Time deposits, also known as term deposits or fixed deposits, are funds that customers deposit with a bank for a specific period, during which the money cannot be withdrawn without incurring penalties. In return, these deposits offer higher interest rates compared to demand deposits.

Features of Time Deposits:

- Fixed Tenure: Funds are locked for a predetermined period, ranging from a few months to several years.

- Higher Interest Rates: Offers better returns than savings or checking accounts.

- Penalties for Early Withdrawal: Withdrawing funds before maturity often incurs penalties or reduced interest.

- Common Types: Examples include fixed deposits, recurring deposits, and certificates of deposit (CDs).

Advantages of Time Deposits

- Higher Returns: Earns higher interest rates, making it an excellent choice for long-term savings.

- Financial Discipline: Encourages disciplined saving by locking funds for a set period.

- Low Risk: Time deposits are considered one of the safest investment options with guaranteed returns.

- Customizable Tenure: Banks offer flexible tenures, allowing customers to choose durations that suit their financial goals.

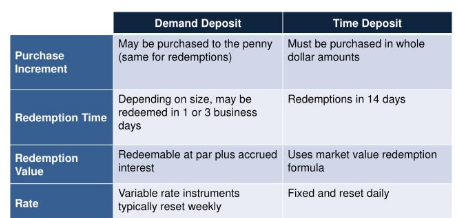

Key Differences Between Demand and Time Deposits

| Feature | Demand Deposits | Time Deposits |

|---|---|---|

| Accessibility | Funds can be withdrawn anytime. | Funds are locked for a fixed period. |

| Interest Rates | Low or no interest. | Higher interest rates. |

| Liquidity | Highly liquid. | Limited liquidity due to withdrawal restrictions. |

| Purpose | Ideal for daily transactions and emergencies. | Suitable for long-term savings and investments. |

| Penalties for Withdrawal | None. | Penalties may apply for early withdrawal. |

Common Use Cases for Demand and Time Deposits

Demand Deposits:

- Personal Finance: Managing daily expenses, such as groceries, utilities, and shopping.

- Emergency Funds: Keeping money readily available for unforeseen expenses.

- Business Operations: Facilitating transactions like payroll, supplier payments, and operational costs.

Time Deposits:

- Long-Term Savings: Setting aside money for future goals, such as buying a house or funding education.

- Earning Interest: Generating passive income through higher interest rates.

- Financial Stability: Diversifying savings portfolios with a low-risk investment option.

How Demand and Time Deposits Impact the Economy

- Liquidity Management:

- Demand deposits ensure a steady flow of money within the economy, supporting consumer spending and business operations.

- Capital Formation:

- Time deposits help banks gather long-term funds, which can be used for loans and investments in infrastructure and development projects.

- Interest Rate Dynamics:

- The balance between demand and time deposits influences interest rates in the economy. Higher time deposits can lead to better returns for savers and stable funding for banks.

Factors to Consider When Choosing Between Demand and Time Deposits

- Financial Goals:

- Choose demand deposits for daily liquidity needs and time deposits for long-term savings goals.

- Risk Tolerance:

- If you prefer low-risk investments with guaranteed returns, time deposits are a suitable option.

- Interest Rates:

- Assess the difference in interest rates offered by banks for savings accounts versus fixed deposits.

- Flexibility:

- Demand deposits offer flexibility for frequent transactions, while time deposits require commitment for a fixed tenure.

- Penalties:

- Understand the terms for early withdrawal from time deposits to avoid unnecessary penalties.

Examples of Demand and Time Deposit Products

Demand Deposits:

- Savings Accounts:

- Earns minimal interest while providing easy access to funds.

- Example: Standard savings accounts in banks.

- Checking Accounts:

- Offers zero or very low interest but supports unlimited transactions.

- Example: Business checking accounts.

Time Deposits:

- Fixed Deposits (FDs):

- Earns higher interest rates for a fixed period.

- Example: A 5-year FD with a 6% annual interest rate.

- Recurring Deposits (RDs):

- Allows customers to deposit a fixed amount regularly for a specified tenure.

- Example: Monthly RD schemes with flexible terms.

- Certificates of Deposit (CDs):

- Time deposits that typically offer higher interest rates but require larger initial investments.

- Example: A 12-month CD with a competitive interest rate.

Advantages of Combining Demand and Time Deposits

Many individuals and businesses use a combination of demand and time deposits to optimize their financial management:

- Liquidity and Growth:

- Keep funds in demand deposits for immediate needs while investing surplus in time deposits for higher returns.

- Emergency Preparedness:

- Use demand deposits for emergencies and time deposits for planned financial goals.

- Diversification:

- Balances risk and return by allocating money across different deposit types.

- Better Financial Planning:

- Helps manage short-term expenses and long-term savings effectively.

Tips for Maximizing Benefits from Demand and Time Deposits

- Shop Around for Interest Rates:

- Compare rates offered by various banks to maximize your earnings.

- Automate Savings:

- Use standing instructions to transfer funds from demand deposits to time deposits regularly.

- Diversify Tenures:

- Opt for time deposits with staggered maturity periods to ensure liquidity when needed.

- Utilize Online Tools:

- Leverage online banking features to manage deposits efficiently and track interest earnings.

Summary

Both demand deposits and time deposits are essential components of personal and business banking. While demand deposits prioritize liquidity and convenience for everyday transactions, time deposits focus on long-term savings and higher returns. By understanding their features, benefits, and use cases, you can make informed decisions to meet your financial goals.